The U.S. consumption train is flying off of the tracks. This is a vital post with essential information for every U.S. and global citizen. It is so important because many still believe in the hope of continued economic and stock market expansion on the back of a strong consumer supported by low gas prices. The facts are that oil is already down 70% and the consumption and jobs data have started to deteriorate. The probability of a low-oil-price benefit overwhelming weakness in the labor market is inconsequentially low. The following writings and graphs illustrate and explain the facts of the unfolding consumption crash.

Firstly and most importantly, joblessness is bound to spike higher as currently the rate of improvement in the labor market is rolling off of its peak. Developing weakness in the labor market was outlined in our last post "job market forecasting depression." Jobs matter because consumers buy more stuff when they gain jobs and buy less stuff when they lose jobs.

As the trend in jobless claims rears its ugly head to the recessionary upside, consumption will decline. These trends are beginning to transpire. The immediate graph below shows the simple truth, with 50 years of data, that when people lose jobs they buy less stuff. Simple analysis of the initial claims and consumption data reveals an r-squared, or a correlation coefficient, of .41. This means 41% of the variability in real consumption can be explained by the change in initial claims.

The evidence is already visible in the data: initial claims and real personal consumption expenditures are reversing trend in the late innings of the business-cycle.

The peak in real consumption growth, which was preceded by the peak in initial claims shrink, has passed.

Meanwhile, production of consumer goods is already on the verge of year-over-year contraction. Producers are seeing the end of the economic expansion and they will need to cut jobs to preserve their profits, which will perpetuate the downward swing in the cycle.

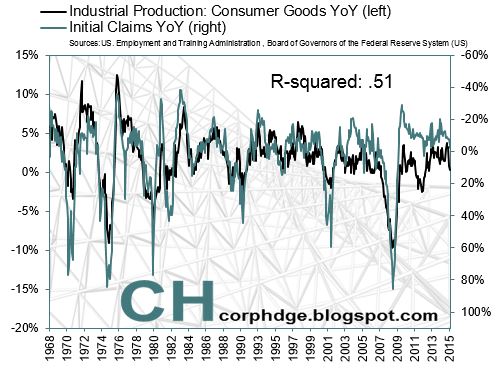

The recent plunge in consumer goods industrial production (IP) growth is likely to further its plunge and head into year-over-year contraction in the coming months.The long-term graph above and the ten year graph below illustrate the leading and predictive reliability of the change in consumer goods IP when forecasting the change in initial jobless claims. While IP of consumer goods contracted in 2011 and 2012, this adjustment was clearly in the early innings of a recovery. The contraction is now much more meaningful as the business cycle is stretched in duration relative to historic standards and jobless claims have begun to reaffirm the weakness in IP.

Zooming in further, we see the reaffirmation clearly. As claims and IP move in tandem, our views of continued declines in the stock market and a recession on the horizon gain further evidence.

Finally, IP of durable consumer goods foretells the crash in consumption. The changes in IP of durables and initial jobless claims represent the flow of the business-cycle over the last 50 years.

Perhaps, nothing indicates the strength of the consumer better than jobs or durable goods trends. That is why the stock market is falling as IP of durable consumer goods growth continues to slow.

Jobs and consumer goods production/consumption measures indicate the consumption economy is on the verge of crashing on its way to business-cycle lows.

No comments:

Post a Comment