With the VIX at 14.02, where it closed Friday, there is 39% downside to the 25 year low of 9.3, 41% upside to the mean of 19.8, and 477% upside to the high of 81.

As the well-respected "tail risk" hedge fund, Artemis Capital puts it, "volatility reflects the difference between the world as we imagine it to be and the world that actually exists." In other words, the general sense of uncertainty is the major driver of volatility and thus of the level of the VIX index.

There are three main reasons the VIX should spike higher: corporate debt is too high relative to sustainable cash flow levels, the economy will weaken more than people think, and the market is at a negative inflection point.

Debt Ratios are High

The business debt to corporate cash flow ratio is above the pre-financial-crisis highs and suggests higher volatility ahead. When debt levels are stretched relative to a capacity to repay debt with cash, the cost of capital rises and equity values become less certain and volatility tends to rise. And the situation is even worse than the graph below indicates.

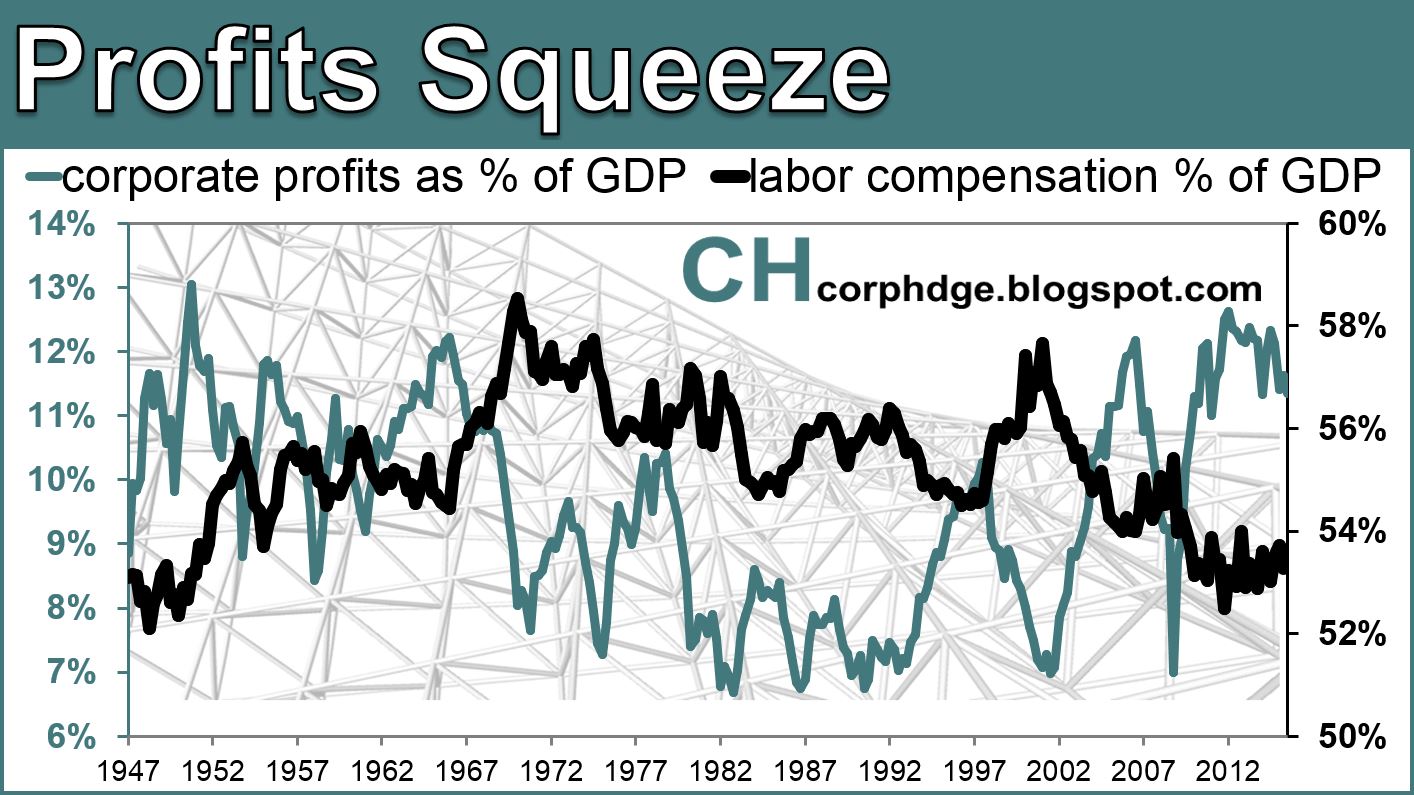

Cash flows are directly linked to profitability, and corporate profits are now rolling off of peak levels as a share of GDP. A continued downward trend in profits is likely and this will boost the debt to cash flow ratio we observe above, as cash flows decline with profitability, and further threaten the certainty of current equity values, which are already expensive on almost every valuation metric versus historic norms.

As you can see, when profits fall, volatility tends to rise. Currently the VIX is too low given the unsustainable level of and the downward trend in profits.

These high profit and debt ratios exist in an environment of zero interest rates. If the Fed continues to raise rates this will only pressure cash flows and profit as more cash is paid in interest. In fact, these issues are already being spotted by the high yield debt market, which is taking it upon itself to raise interest rates on companies of shaky credit quality.

Although the recent pullback in yield spreads has knocked down the VIX, my analysis indicates this is unsustainable. The correction in spreads has not altered the upward trend and the recent move lower has been driven by a false belief in higher economic demand, which I will explain further along in this post.

Over time, volatility and the high yield spread track along with each other. And, as I explained earlier, debt levels are too high at a time when corporate profits are rolling off of unsustainable highs and policy guided interest rates are already at zero creating a dire outlook for equity values and certainty of those equity values.

Growth Expectations are Wrong

It looks like the recent slam down in volatility was driven by a reflation trade mistaken for a true economic demand revival. Deflation has been the persistent market risk as commodity prices have fallen. Commodity producers built capacity with cheap money based on high expectations of economic demand. As demand has undershot to the downside of expectations, deflating commodity prices have reflected this demand letdown. A recent move up in inflation expectations, as seen in breakeven rates, lead the market up and drove volatility down.

This move in inflation expectations is reasonable given the bouts of quantitative easing and negative interest rates enacted by the European and Japanese central banks and the implication for US policy rates/easing measures from here on out. The main difference between what the market is doing and what is correct, is that the move higher in inflation expectations should not be based on true economic demand or a "pull" type inflation, which is the only thing that would be positive for corporate profits and market certainty at this point.

Economic uncertainty leads to market uncertainty, as shown below with the relationship between the change in jobless claims and the VIX.

As explained in "Job Market Forecasting Depression", the rate of job-losses is at historic lows and is set to rise, and when this transpires volatility will spike higher.

Market Inflection Point

Uncertainty is greatest when markets are falling. The following charts show the S&P 500 starting to roll over. Historically, when markets rollover like this after such a long bull run and the economic fundamentals such as jobs and corporate profits weaken, as I explain they should, uncertainty increases and prices fall quite drastically.

The market appears to be entering a new downtrend with accelerating volume, as was the case in the prior two major market crashes or corrections.

Accompanying this inflection point downwards in the market should be high uncertainty and high levels in the VIX index, but the VIX is below average and is near historic lows!

This is a unique opportunity. Volatility should be higher given that corporate profits are rolling off of peak levels, debt to cash flow ratios are near all-time highs, policy rates are at zero and expected to rise, job-losses will increase, and the market is at a turning point after a long bull market. Meanwhile, the VIX currently offers more upside to merely its historic average than it does downside to its 25 year low.

Sources:

Federal Reserve database, federalreserve.gov, BLS, BEA,

Chicago Board Options Exchange, Artemiscm.com

AM